(888) 513-3010

(888) 513-3010To schedule a free case evaluation with our Florida stock fraud attorneys, please contact Colling Gilbert Wright today. Located in Orlando, our attorneys help victims of fraud throughout the country.

Banks Underpricing Corporate Bonds by 18 billion?

A new study says there’s a flaw in the process for selling new debt issued by companies.

By Tracy Alloway, Bloomberg News

The process of pricing and selling new corporate bonds has often been described as more art than science. But a new paper from London-based research firm Fideres Partners LLP suggests it may just be inaccurate. “Corporate bonds’ price in the days after their issuance may hint to a systemic under pricing by major dealers,” Fideres, which has previously researched the rigging of the Libor benchmark interest rate, wrote in new research published this week. The firm estimates that the under pricing of new debt may have cost U.S. companies as much as $18 billion in extra interest in bonds issued between 2010 and 2015 by ratcheting up their borrowing costs at a time when benchmark interest rates were at ultra-low levels.

The study comes as the process by which new bonds are sold has already caught the interest of U.S. and European regulators in light of the rampant bull run in corporate debt. Companies have been racing to sell new bonds to take advantage of low interest rates and eager investors, creating a fee bonanza for bankers who sell the debt and increasing the size of the overall U.S. corporate debt market from $5.4 trillion outstanding in 2009 to $8.1 trillion currently.

When issuing bonds, companies typically hire syndicate bankers at large dealer-banks who are charged with gaging demand for such debt, estimating a good price at which to sell the resulting securities, and identifying clients who might be their best buyers and holders. Such bankers must weigh a variety of factors in their decision-making and sometimes may under price new bonds in order to make sure they end up in the portfolios of large ‘buy and hold’ investors who are seen as more dependable. So-called ‘concessions’ on new issues may also arise as investors and banks involved need to be compensated for the extra risk of holding corporate credit as opposed to safer securities such as U.S. government debt.

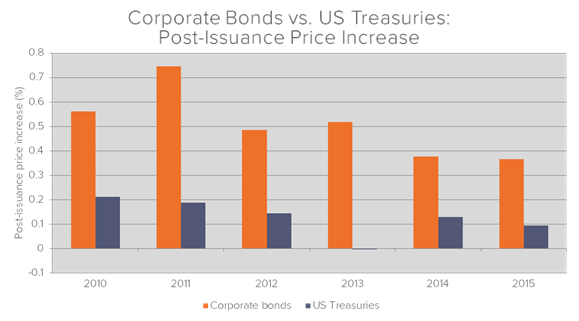

Fideres found that the price of corporate bonds typically increases by 0.50 percent between the day the price of the new debt is announced and the day it’s sold, compared to a 0.15 percent rally in newly-issued U.S. government bonds in the same time frame. Bonds sold by junk-rated companies with more fragile balance sheets tend to increase by 1.5 percent, while top-tier investment-grade corporate debt enjoys just a 0.40 percent rally.

The chart below shows how corporate bonds tend to increase in value far more than U.S. Treasuries do soon after they’re issued:

The new issue pop, Fideres said, isn’t as strong when it comes to the corporate bonds issued by big banks themselves. “As an aside, Fideres also performed some preliminary analysis that shows that dealers actually have a good track record of pricing their own bonds in a competitive manner so that they minimize the premium that they pay to the market,” the research firm wrote. The average price jump shortly after such bonds’ announcement date is about 0.30 percent, compared to the 0.50 percent seen by the wider corporate debt universe, the firm noted. Results, however, may be skewed as big banks tend to be large issuers of debt and so may enjoy a premium compared to some other types of companies.

Fideres partner Alberto Thomas suggested bankers may be dealing with conflicts of interest: They need to find the best borrowing deal for companies while satisfying the interests of some of their biggest clients. Clients that receive big portions of popular new debt, including banks which often hold parts of new issue programs to help provide liquidity in the secondary market, can immediately record a paper gain on the new debt.

“Because of their relationships with both the issuer and investors, dealers face pressures from both sides and the outcome will partly depend on the relative strength of these forces,” Fideres, which often prepares research materials for use in class action lawsuits, said. “The potential mis-pricing of bonds is driven principally by an asymmetry of information. The dealers who manage the syndication of the bonds know the level of demand from investors but the corporations who issue the bonds generally do not.”

If you have been the victim of securities fraud, no matter if a pending criminal suit is underway, the stock fraud and FINRA attorneys at Colling Gilbert Wright can help. With decades of combined experience, our attorneys are here to take your case and fight for your rights, helping ensure you are properly compensated for your damages.

More Articles For You...

April 9, 2016